|

| Assuming a Pre-existing Mortgage |

An Assumption of Mortgage occurs when you you purchase a home and

assume the seller's pre-existing mortgage. You're then required to

fulfill the obligations of the existing loan agreement the seller made

with the lender. The obligations are similar to those you would incur

if you were taking out a new mortgage. When assuming a mortgage, you

become personally liable for the payment of principal and interest. An Assumption of Mortgage occurs when you you purchase a home and

assume the seller's pre-existing mortgage. You're then required to

fulfill the obligations of the existing loan agreement the seller made

with the lender. The obligations are similar to those you would incur

if you were taking out a new mortgage. When assuming a mortgage, you

become personally liable for the payment of principal and interest.

The

seller remains liable to the mortgage lender (whether the lender is

a commercial bank, credit union, thrift, mortgage banker, or mortgage

broker) until the lender agrees to release them. When the seller, or

original mortgagor, is released from the liability, they should get

that release in writing. Otherwise, he or she could be liable if the

new owner doesn't make the monthly payments.

For

example, a homeowner owes a 30-year mortgage loan of $250,000 against

his house. A prospective buyer wants to purchase the house and assume

the pre-existing mortgage. The buyer pays $50,000 cash for the equity

and assumes the mortgage, becoming liable for the debt. The original

owner remains liable as well if he or she is not officially released

from the agreement with the lender.

|

|

Click here to view an example of an Assumption of Mortgage Agreement Form

|

|

|

| What is a lease option and when is it right for you? |

|

A lease option basically means you are

leasing or renting a property with an option to buy it at a future date.

The future price of the property should be fixed at the time the

lease-option is signed. A lease option basically means you are

leasing or renting a property with an option to buy it at a future date.

The future price of the property should be fixed at the time the

lease-option is signed.

Usually there is an up-front payment of

some amount to purchase the option. That amount can vary.

Sometimes the monthly payment is larger than normal and the excess is

used to purchase the option. In some cases, the option money can

be applied toward the down payment for the later purchase of the home.

Lease-options are usually done during a slow real estate market.

During a hot market, the seller can simply sell the home in the regular

manner.

What benefits do a lease option hold for the seller?

- They often get to sell the house at a higher price than they

could sell it in a normal transaction.

- They can sell the house during a slow market.

- By being able to collect a larger

monthly payment than they could obtain in a normal lease, the

property "cash-flows" and they don't have to come up with

money out of their own pocket each month to make the mortgage

payment.

- They get some up-front option money

and when the buyer cannot exercise the option, they get to keep it.

What risks do a lease option hold for the buyer?

Individuals who attempt to

buy homes on a lease-option rarely end up buying the home. This

often has to do with the reason they try to buy on a lease-option.

They usually cannot qualify for a home loan and expect that they will be

able to qualify after a period of time. Later, they find they

still cannot qualify - whether it is because of poor credit, lack of

income (documentable income), or lack of savings to have a large enough

down payment. If this happens, you lose any option

money you might have paid up front or as part of your monthly payment.

|

|

Read more....

|

|

|

| Is buying commercial property for income a good idea now? |

Buying commercial real estate can be a secure and profitable investment

if you take the time to research, get advice from experts and know your

risks and benefits. Buying commercial real estate can be a secure and profitable investment

if you take the time to research, get advice from experts and know your

risks and benefits.

"There are four main reasons to buy

investment real estate: cash flow, appreciation, depreciation and

principal pay-down," says Mike McCaffery, Investment Property

Consultant, GFS Commercial, a division of the Guiltinan Group Real

Estate Specialists.

Owning commercial real estate can be a great

way to diversify your portfolio, create tax benefits and build wealth.

However, buying commercial real estate can be a risky business,

especially these days when many people are getting into real estate

without completely understanding the industry.

"There are

different kinds of investors. There are some people who are very

wealthy and they'll buy trophy properties for example and the returns

are very minimal, but they hold them because they want to have a

long-term hold. A lot of other investors want the cash flow so they're

going to go to other areas that have a higher cash flow or higher

return but it's not going to be in the best areas," says Investment

Property Consultant Eric Warfield with GFS Commercial.

|

|

Read More...

|

|

|

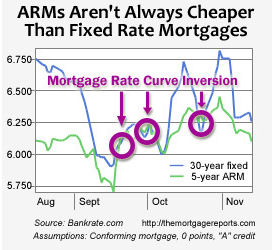

| Which Is Better: Fixed Rate Mortgage Or Adjustable Rate Mortgage? |

People often assume that because adjustable-rate mortgages "share risk"

between mortgage lender and mortgage lendee, they will be rewarded with

a lower mortgage rate than if they chose a comparable fixed-rate

mortgage.

The chart at the left proves that thinking false. The chart at the left proves that thinking false.

Three

separate times since mid-September, 5-year ARMs priced worse than a

similar 30-year, fixed rate mortgage. It's atypical, but it does

happen from time to time.

And it's also why locking mortgage

rates is like running a Peyton Manning offense -- you can't call a play

until you've stepped to the line and studied what's on the other side

of the ball.

Before settling on a specific mortgage plan,

remember that mortgage markets change daily and mortgage rates change

every 3 hours, 11 minutes. A 5-year ARM may look cheaper in the

morning, but by the afternoon, it could be losing out to the 30-year

fixed and -- all things equal -- it's better to take that fixed-rate

mortgage at a lower rate if it's available.

|

|

Read More...

|

|

|

John FriedmanKeller Williams Realty(866) 333-5555WebsiteEmail

|

|

|

|

|

|