State & Federal Taxes take a big chunk out of your wages, bonuses, and investments. If you also happen to be a business owner, taxes can eat up a big portion of your company's profits. Every year checks must be written to the U.S. Treasury for federal income taxes, Social Security, Medicaid, and to the state treasury in the state you reside for state income taxes. Let us not forget we also pay real-estate taxes, sales taxes, and an additional luxury tax on certain vehicles and goods all with money that has already been taxed. Total taxes paid can easily eat up half your income if you don't take action to stop it.

By now you are probably wishing you never opened this email and you may feel ill just thinking about the painful financial burden of taxes on your life. Well, I completely understand your frustration. What is even more alarming is that most people never take action and continue to write checks to our friends in Washington DC. Another incredible fact is that most people don't know that paying taxes in retirement is optional. That is correct, you do not have to pay the majority of these taxes in retirement. However, this can only be accomplished with professional planning and making the changes we recommend in a customized financial plan.

Do not panic, there is good news for you in this Special Report on taxes. QCI can alleviate the systematic and aggressive destruction of your wealth. I encourage you to put into practice these 12 basic steps to keep Washington DC from taking a big bite out of your wallet whether you are a individual earner or business owner.

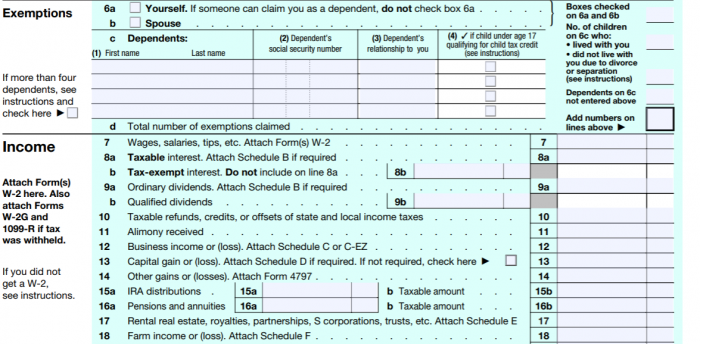

Step 1 - IRS Form 1040, Line 8a- Taxable Interest Income

Taxable interest income increases your tax liability. Tax deferred vehicles such as indexed annuities are safe and secure and will reduce this liability. If structured properly, you can have tax free income for the rest of your life at retirement that is both safe and secure. Have you ever considered an indexed annuity ?

Step 2 - IRS Form 1040, Line 9a & 9b, Ordinary & Qualified Dividends, Capital Gains

Short term capital gains and ordinary dividends are taxed at the higher ordinary income tax rates. Should your ordinary dividends be qualified and taxed at a much lower rate? Should the gain be converted to longer term treatment or be deferred in a different vehicle such as an annuity ?

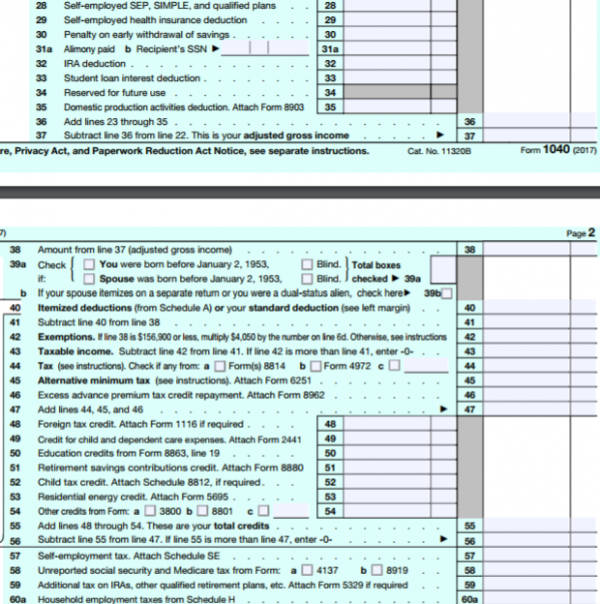

Step 3 - IRS Form 1040, Line 28 Self-employed qualified plans (See Sample 1040 below)

QCI can assist you in creating the most tax efficient self-employed high deductible plan for your business. Have you considered deducting up to 75% of your income? Yes, that is was not a typo! We can set up customized plans where you can deduct more than half of your income and reduce your income taxes by more than 50% in most cases.

Line 32-IRA Deductions

Are you taking full advantage of all IRA deductions available to you? Are you aware of catch up contributions and deductions for those over 50 years of age?

Step 5 - IRS Form 1040, Line 40 - Itemized deductions

Have you considered a lifetime gifts to your favorite charity? With the use of life insurance and a charitable remainder trusts, you can make current deductible gifts to your charity and lower your taxes. Best of all you retain a lifetime income for yourself, but not disinherit your heirs. Are you interested in learning how this works?

Step 6 - IRS Form 1040, Line 59 - Tax on IRAs

Pulling money out of your IRA before the age of 59 1/2 can create a 10% penalty by the IRS. Did you know that 85% of your social security check will be taxed if you pull out too much money from your qualified accounts? Did you know that as a result this can increase your monthly payment of medicare insurance by 50%? Have you considered obtaining lifetime income that is tax free to avoid the increase in taxes on your social security benefits and increase in monthly Medicare premiums?

Step 7- IRS Form 1040, line 63 - Total Tax

Are you currently maximizing your deductible contributions into your employer sponsored retirement plans such as 401k, 403b, or 457 plans? If you are contributing the max, have you considered a personal supplement non - qualified retirement plan?

Step 8 - Minimum Required Distributions from IRAs (RMDs)

If you are over the age of 70 1/2 and do not want to pay higher taxes due to forced RMDs, the government now gives you the option of deferring further up to $125,000 of your IRA assets with a Qualified Longevity Annuity Contract (QLAC). We can help you start the process of applying for a QLAC to reduce your income taxes during retirement.

Step 9 - Roth Conversions

By April 15th 2017, the time has passes to covert traditional IRAs to Roth IRAs. However, Roth conversions that did occur prior to April 15th 2017 have until October 15th 2017 to re-characterize the Roth Conversion back to a Traditional IRA. Typically, this would occur only if the account suffers significant investment losses, or the taxpayer incurs substantial economic hardship.

Did you know that using a combination of a Roth conversion in conjunction with an index annuity can both reduce the impact of taxes on the conversion and provide a lifetime income that is both tax free for life and secure? Have you considered a Roth conversion for tax free lifetime income?

Step 10 - 60 day IRA Rollover

When a taxpayer takes personal receipt of qualified funds from a 401k, IRA or other qualified plan, they have 60 days to roll these funds into an IRA or other qualified plan. Note, that occasionally the Secretary of the Treasury can waive this requirement if uncontrollable events occurred to the taxpayer to make this impossible, such as natural disaster, military activation or serious illness.

Step 11- Substantial Equal Periodic Payments (SEPP)

When a taxpayer begins taking a distributions from an IRA or other qualified plan before age 59 1/2, a 10% penalty could apply. To avoid this penalty, IRC, Section 72, allows SEPPS to be withdrawn by the taxpayer.

Once begun, the taxpayers must continue the payments for at least five years or until after age 59 1/2, whichever is longer. Occasionally, taxpayers will neglect to continue the payment stream, especially if the income stream is no longer needed. but this may trigger the original penalty.

Step 12- Personal Net Worth

Many people use this time of year to review their overall financial net worth. If your clients have a family and heirs they wish to protect, life insurance is still the best way to protect assets or future earnings potential. Have your assets increased and need more protection?

Have your assets decreased and need less insurance? If you need less insurance we can turn the cash value into a tax free income stream. Lapsing or surrendering a life insurance policy will create a tax bill if your cost basis is below total premiums paid plus the growth. There is a better way to turn life insurance into tax free income during life. Talk to us here at QCI so that we may discuss a 1035 exchange in order to tap into the cash value tax free.

At QCI, we have a tremendous suite of quality financial instruments and tax-lowering strategies available to help you reach your long-term financial goals. The foundation of your retirement begins with the financial planning process. While it might take an hour of your day in gathering the data we need to get your customized plan created, the total lifelong value is immeasurable. With our complimentary ($5,000 value) award winning financial planning tool, Money Guide Pro, we can construct a solid, dynamic financial plan that can assist you in achieving your financial retirement goal that is both secure and free from excessive taxation.

Kindest Regards,

Joshua E. Betancourt, MSA

Chief Portfolio Strategist/Financial & Tax Planner

Quantum Capital Investment Inc.

Joshua@Quantumcapitalinvestments.com

All written content is for information purposes only. Opinions expressed herein are solely those of “Quantum Capital Investments” and our editorial staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. Fee-based financial planning and investment advisory services are offered by “Quantum Capital Investments” a Registered Investment Advisor. Insurance products and services are offered through “HST Insurance brokerage and JDS Life insurance brokerage.” “Quantum Capital Investments” and "HST and JDS insurance brokerage” are affiliated companies. The presence of this web site shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services.

|